Identifying opportunities and its ability to deploy its capital at pace is crucial for LMS to scale to the next level. Despite the impending revenue leap above RM$100mil, growth has been funded without leverage. This leaves tremendous balance sheet potential to scale its revenues into $500mil bracket. 30% Prismatic free option on Malaysia’s landslide protection market (TAM RM$100mil).

LMS Compliance (LMS) is the dominant asset protection provider in Malaysia, commanding xx% market share of $22bn sector revenue (80% independents, 5% other large consolidators).

Recent acquisitions are well thought out.

Identifying opportunities and its ability to deploy its capital at pace is crucial for LMS to scale to the next level. Despite the impending revenue leap above RM$100mil, growth has been funded without leverage. This leaves tremendous balance sheet potential to scale its revenues into $500mil bracket.

LMS mgt maximizes shareholder value (SHV) via (i) div yield circa $2mil (or 5.2%), (ii) annual FCF generation of $90mil (x% yield) and (iii) maintaining medium term growth rate of 10% for base-case total shareholder return (TSR) of xx%.

LMS low beta of 0.301 makes it ideal for portfolio allocation. Mgt foresight for value-accretive acquisitions for new market shares reinforces SHV creation.

6Σ estimate intrinsic value at $xx, equivalent of global TIC exit yield at xx.

George KOH

george.koh@rhtgoc.com

Research Director

Paul SCHYMYCK

Paul.schymyck@rhtgoc.com

Research Director

Mkt cap: $54 mil [$0.40 27Feb26]

Intrinsic Value: $1.00

10 day adtv: ?m

Singapore

Industrials, Commercial & Professional Services [2020]

Testing, Inspection and Certification services

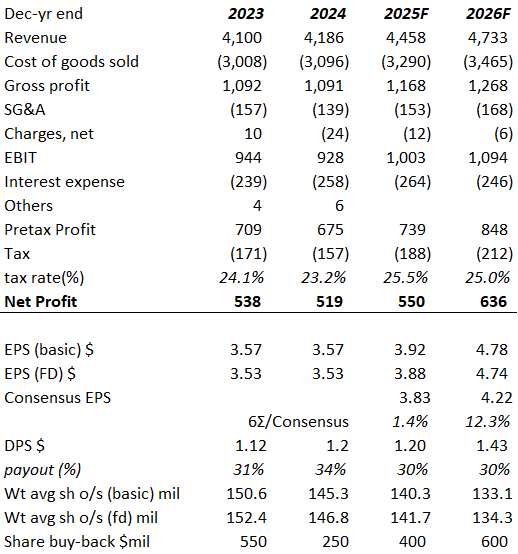

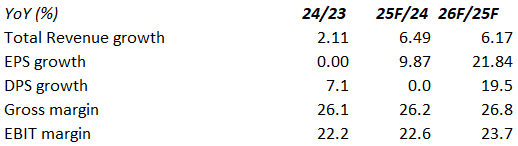

| RHTC Forecast | 12/23 | 12/24 | 12/25F | 12/26F |

|---|---|---|---|---|

| Revenue $mil | 4,100 | 4,186 | 4,458 | 4,733 |

| Consensus | 4,300 | 4,450 | ||

| Rev$m | 944 | 928 | 1,003 | 1,094 |

| EBIT $mil | 538 | 519 | 550 | 636 |

| Net Income $mil | 3.53 | 3.53 | 3.92 | 4.70 |

| EPS ($) | 3.53 | 3.53 | 3.88 | 4.66 |

| EPS fd ($) | 3.83 | 4.22 | ||

| Consensus EPS | 23.7 | 23.7 | 21.5 | 17.6 |

| ($) | 2.17 | 0.81 | ||

| P/E (x) | 21.6 | 22.5 | 32.3 | 40.9 |

| PEG (x) | 33.4 | 32.2 | 33.3 | 37.6 |

| Rule 40 (%) | 1.34 | 1.44 | 1.44 | 1.76 |

| ROAE (%) | 140 | |||

| Div Yield (%) | 71% | |||

| Intrinsic Value % upside | ||||

| Source: RHTC est |

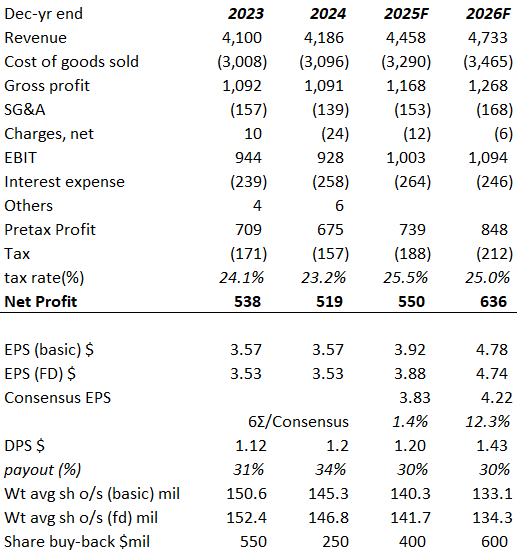

||||

| Industry Valuation [CNBC 5yr beta] |

PE 2026F |

Div Yield 256(%) |

BETA12 | Mkt Cap $mil |

|---|---|---|---|---|

| LMS | 21.5 | 1.76 | 0.30 | 60 |

| Intertek [0.87] | 9.10 | nil | 0.46 | 210 |

| SGS | 11.15 | nm | .81 | 579 |

| Buena Vista | 6.49 | 0.13 | 0.57 | 196 |

| STI | 9.27 | 0.14 | 0.28 | 73 |

| 1: YTD calculated beta to S&P, 2: Factset, 3: fund prospectus | ||||

Day

Price $0.38

Ratios & Valuations _____________

Growth & Margins (%) ______________________

Income Statement $mil _____________________

Balance Sheet $mil ____________________

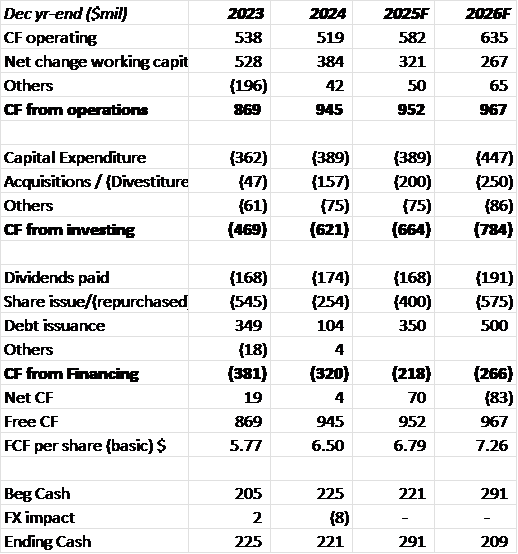

CashFlow $mil __________________________________

CashFlow $mil __________________________________

EXECUTIVE SUMMARY

We met with CEO Dr Louis Ooi prior to initiating our report on LMS Compliance (LMS). We are impressed with management’s depth of knowledge on the Testing, Inspection and Certification (TIC) cycle and its pursuit of excellence. We visited its newly renovated laboratory in Johore Bahru, Malaysia (the other 2 located in Kuala Lumpur and Penang) akin to a well-funded Top Tier University Science Lab equipped with latest diagnostic & testing equipment. We discussed key issues such as its growth strategy, how LMS is scaling up to the next level (revenue >$100mil), its positioning for further upscaling (towards $500mil milestone), outlook and opportunities on TIC + Assessment market, LMS ability to consolidate its above-industry margins and its recent foray into China.

We have strong expectations of LMS foothold into China. The 75% subsidiary ACC has captured substantial market share in Chinese Novel food exports into USA, which requires product compliance with strict licensing and FDA guidelines for approvals. Based on Chinese Novel protein exports to US of $440mil (2024), we estimate the implied recurring revenue contribution circa RM$15mil (with conservative >10% growth). This implies acquisition ROIC circa 30% and equivalent to 5% mkt cap. We anticipate substantial upside risks on reverse Novel food imports into China as exporters seek experienced and bilingual service providers. Singapore could potentially be another Novel growth market for LMS.

Another related growth market is the potential new EV certification for imports into Malaysia. This vehicle Inspection growth appendage has TAM of RM30mil with 30% CAGR and its asset light model supports pre-tax margins of at least 30%. We estimate if LMS were able to secure accreditation for new EV import inspection, this could add between RM5-7mil in PBT (or S$2cts per shr or 5% mkt cap).

Water certification for Data Centers in Malaysia. LMS is well positioned with its labs location in Penang (mature semi-conductor industry), KL (govt designated Super Corridor Multi-Media highway) and JB (increasing new Data Center concentration). Recent Anwar government announcements that Malaysia will only allow AI-Data Center construction (higher project development costs) due to heavy demands on water and electrical infrastructure. LMS is well positioned to tap into the DC demands for water testing & certification. We estimate a recurring EPS impact between 2-5% of mkt cap.

Water certification for Data Centers in Malaysia. LMS is well positioned with its labs location in Penang (mature semi-conductor industry), KL (govt designated Super Corridor Multi-Media highway) and JB (increasing new Data Center concentration). Recent Anwar government announcements that Malaysia will only allow AI-Data Center construction (higher project development costs) due to heavy demands on water and electrical infrastructure. LMS is well positioned to tap into the DC demands for water testing & certification. We estimate a recurring EPS impact between 2-5% of mkt cap. <br>

Slope mgt. Associate contribution between RM5-9mil (or 5% of mkt cap). We are highly conservative in estimating

LMS Compliance listed on the Singapore Exchange Catalist Board in December 2022, raising S$3.64 million through a fully subscribed IPO at S$0.26 per share , marking its transition from a regional Malaysian laboratory to a comprehensive ESG assurance platform. LMS achieved exceptional 32.5% revenue growth in FY2025 with a robust 28.0% PBT margin, significantly outpacing the 3.9%-8.1% organic growth rates of mature global peers while maintaining pristine balance sheet strength with a net cash position. The $4.51 million acquisition of Anchor Technology Holdings represented 11.25% of LMS’s market cap and immediately drove a 29.8% surge in net profit , demonstrating aggressive M&A deployment relative to scale compared to the more conservative 1.5%-6.3% market cap acquisitions by global competitors. Customer retention rates in the TIC sector hover between 75-80%, with clients rarely switching providers unless experiencing severe service failures , creating powerful incumbency moats that favor established global players with comprehensive geographic footprints and accreditation portfolios. LMS maintains a lean 7-member board with 57.1% independence and strong 42.9% gender diversity, led by co-founders with 19 years of industry tenure , contrasting with the larger 9-13 member boards and tenure-capped governance structures of multinational peers. LMS built its IP strategy around proprietary cloud applications including aikinz-LIMS and aizenz, relying on software copyrights rather than hardware patents, reporting zero formal patent filings in FY2023 , while global peers hold €461.5M-£329.4M in intangible assets and pursue hardware-focused patent portfolios .

LMS trades at a competitive 19.20x P/E ratio with a 3.80% dividend yield , valued between the premium 22.86x multiple of SGS and the discounted 16.07x valuation of Intertek , reflecting investor recognition of its high-growth profile despite its smaller scale.

2. OVERVIEW

Executive Summary

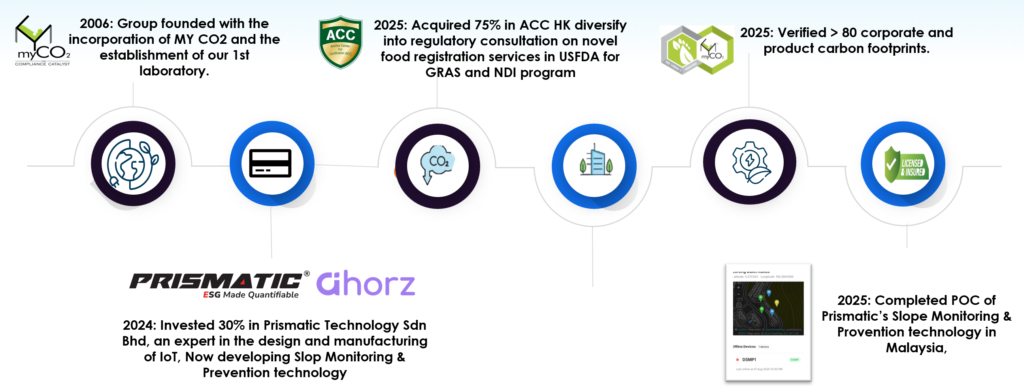

LMS Compliance was co-founded in 2006 by CEO Dr. Ooi Shu Geok and Ms. Chong Moi Me with the primary goal of enhancing consumer trust in homegrown Malaysian brands. The company launched its first laboratory at a time when local businesses often viewed testing and certification as an unnecessary expense rather than a vital tool for earning consumer confidence. By 2007, LMS began developing its proprietary Laboratory Information Management System (LIMS), which served as an intelligent digital backbone for automating data capture and compliance workflows.

As at Sep 2016, the company offers more than 1,100 accredited tests and 10,200 non-accredited tests (Business Times 22-Nov-2022). LMS achieved early industry milestones, notably becoming one of the first local private laboratories in Malaysia to conduct toy safety testing compliant with the Ministry of Domestic Trade and Consumer Affairs standards. [5] During the COVID-19 pandemic lockdowns, the management team successfully pivoted by launching face mask testing services that complied with ASTM and EN specifications, providing a crucial revenue stream during the crisis.

On December 1, 2022, LMS Compliance officially commenced trading on the Catalist Board of the Singapore Exchange Securities Trading Limited (SGX-ST). [7] The successful initial public offering involved a fully subscribed placement of 14 mil shares at S$0.26 per share, raising approximately S$3.64 mil to fund regional expansion and synergistic acquisitions. [8] Following its public debut, LMS was able to upscale its traditional laboratory testing company to a serious asset protection firm with international ambitions.

To support its organic growth operations, the company significantly expanded its physical footprint, completing a major 15,000-square-foot laboratory upgrade in Shah Alam (Kuala Lumpur) and expanding its Johor Bahru facility in 2024. [10] In May 2024, the group acquired a 30% stake [RM$54mil] in Prismatic Technologies Sdn Bhd [section 2-3-2] to bolster its automated data generation capabilities for sustainability reporting.

Figure 2-1: Milestones

Source: LMS

The company accelerated its inorganic growth strategy in July 2025 by completing the US$4.5 million acquisition of a 75% stake in Anchor Technology Holdings Co., Limited (ACC) [section 2-3-1]. In October 2025, LMS further broadened its ecosystem by incorporating MY CO2 Inspection Sdn Bhd [section 2-3-4] to capture emerging opportunities in electric vehicle and goods inspection services.

Current Asset Protection Portfolio Composition

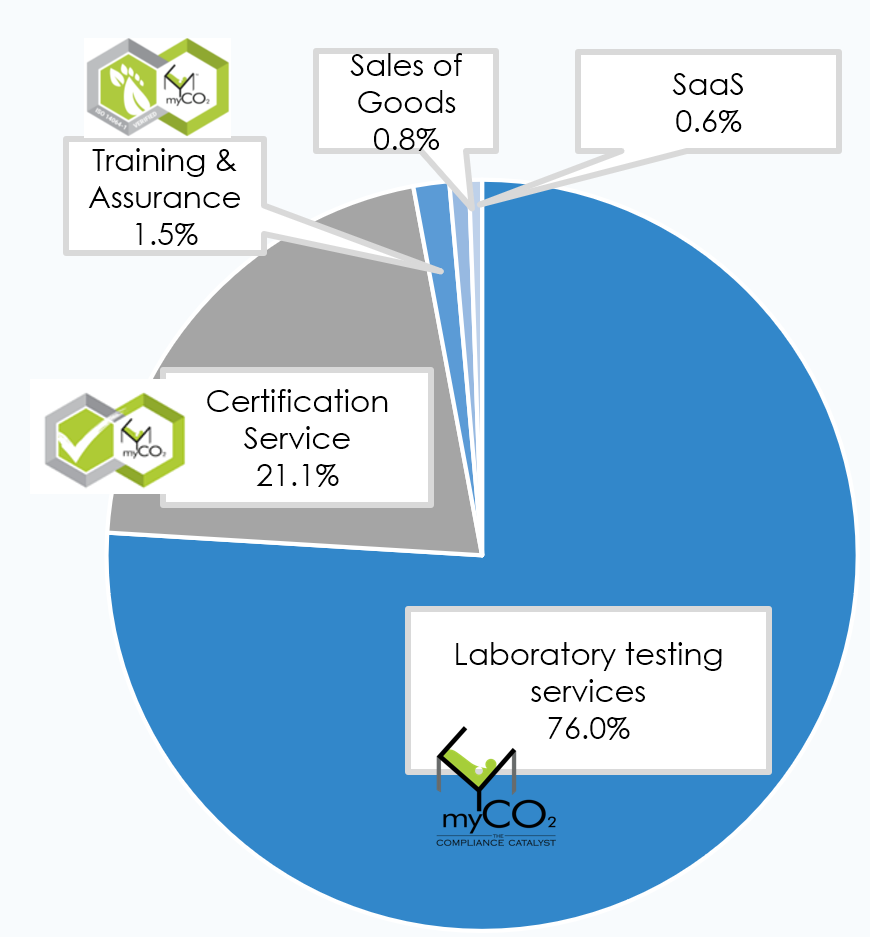

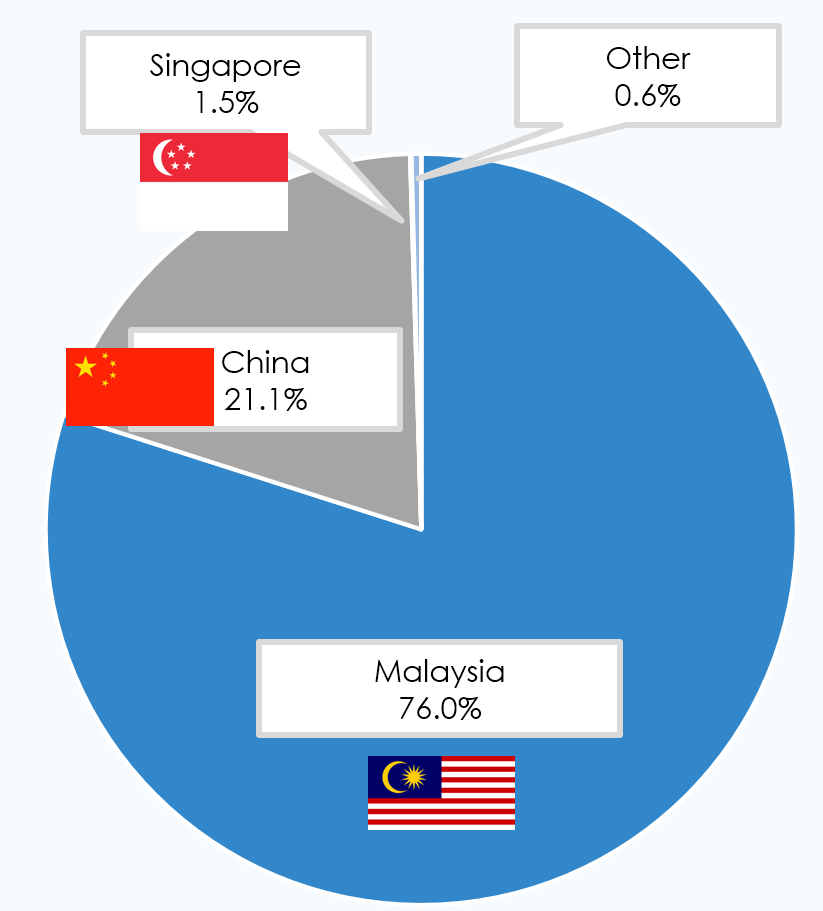

LMS has established itself firmly as a serious TIC industry player with more than 20 years of operational experience. Over 80% of the Group’s revenue coming from its testing and assessment segment attributable to repeat customers.

Figure 2-2: LMS Fy2025 revenue composition

LMS Compliance currently operates through five primary business segments, which together form a fully integrated compliance and assurance ecosystem.

- Testing and Assessment: Through its ISO/IEC 17025 accredited laboratories, the group provides chemical, microbiological, nucleic acid and physical analyses to assist customers in achieving compliance with industry standards and ensure consumer product safety. While historically the dominant revenue driver at over 95%, this segment accounted for 75.96% of the group’s total revenue in FY2025 as other divisions expanded.

- Certification and Consultancy Services: Operating as an ISO/IEC 17021 accredited body, this segment conducts audits for quality management (ISO 9001-2015), food safety (ISO 22000-2018, MS 1480-2019) and occupational health systems (ISO 45001). Driven by the strategic acquisition of ACC, this division’s revenue contribution surged to 21.10% in FY2025.

- Assurance, Validation & Verification: Introduced to address the global green economy transition, this segment provides comprehensive ESG data collection, impact assessment, and greenhouse gas reporting services. The group’s subsidiaries hold dual accreditations as Validation and Verification Bodies (VVB) from both the Singapore Accreditation Council and the Department of Standards Malaysia.

- Conformity Assessment Technology (SaaS): The company markets its proprietary cloud applications, including “aikinz-LIMS” for digitizing laboratory operations and “aizenz” for streamlining ISO certification processes.

- Trading: This segment is dedicated to the distribution and trading of a broad range of analytical instruments, scientific testing equipment, and laboratory consumable items, contributing 0.8% of FY25 revenue.

Client Group Exposure by Industry

LMS Compliance maintains a diversified client base across a broad spectrum of heavily regulated industries.

Figure 2-3: LMS clients across 10 countries

| 2025 revenue composition | Industries and geographical exposure |

|---|---|

|

|

LMS testing services allow businesses, their customers, regulators, and other stakeholders to assess the quality and safety of products or materials, validate whether the manufacturing process is achieving its intended outcomes, and check for compliance with the applicable standards and regulations.

The core testing and assessment services cater primarily to the food, feed, fertilizer, pharmaceutical, medical devices, healthcare, industrial and green-tech sectors. The strategic acquisition of ACC specifically broadened the group’s capabilities and client exposure within the novel food and dietary supplement sector. Furthermore, the establishment of the new inspection subsidiary allowed LMS to penetrate the electric vehicle market. Through a strategic collaboration with the Malaysian Semiconductor Industry Association, the company also provides ESG

2-1 Strategy

2-1-1 New Business Growth {DC, EV}

Exec Sum – Leveraging into Malaysia’s Data Centre growth (estimated Biz worth x yrs of growth)

EV inspection (estimated Biz worth x yrs of growth)

2-1-2 LMS Acquisition strategy {Prixmatic, ACC HK}

The acquisition of a 30% stake in Prismatic Technologies Sdn Bhd [May 2024], specialising in automated data generation for sustainability reporting companies and organisations focused on sustainable buildings and environmental impact assessments, paving the way for technological advancements and the Company’s service diversification. As 1 of 6 Prismatic product offerings, we highlight Earth Slope Monitoring (Detect ground movement and structural instability to prevent landslides and accidents) as a potential game-changer [section 2-3-2]. With an estimated TAM of xmil, a 30% market share would result in $ biz value for LMS.

2-2 Current Business Model (APS)

2-2-1 Geographic Exposure

27-Jan-25 announced a 75% acquisition of Anchor Technologies (HK), who has substantial market share in Novel Food Chinese export certification to USA (see section 2-3-1). Funded with cash raised during IPO and issuance of new LMS shares, this acquisition marks a new geographic footprint for LMS expansion.

2-2-2 Customer Base & Demand Drivers

[Dec-2024] LMS forged a collaboration with the Malaysian Semiconductor Industry Association, Masverse Technologies Sdn Bhd, and CRIF Omesti Sdn

APPENDIX A1 – SWOT ANALYSES

| SWOTs | Description [Report section] | Probability / Risks |

|---|---|---|

| Strengths |

*Leverage on expertise accumulated over 20 years TIC to penetrate new markets and maintain market share/margins *Low Balance Sheet gearing insulate against any macro downturns |

HIGH Medium-High |

| Weakness | Limited Executive Management Resources may curb next stage in scaling revenue growth (RM150-300mil level) | Low-Medium |

| Opportunities |

|

High Medium-High Medium-High High |

| Threats |

Potential of established global TIC companies competing for LMS’ new market opportunities:

|

Low – Regulators preference Low Low – Regulators preference Low – Completion of POC |